Systems and markets and dysfunction

The duality of NEM

If you live in one of the southern Australian states, you will have noticed that our fairly mild winter recently took on a rapid chill.1 And with the plunging temperatures came some familiar contours – tight supply and demand conditions across the NEM produced spot price volatility. In fact in the last fortnight we’ve had some biiiig price volatility.

EnergyByte wrote up an excellent blow by blow coverage of the extended volatility seen on Wednesday 11 June and Thursday 12 June, and Thursday 26 June. They noted that the volatility on Thursday 12 June “delivered 5 of the top 6 highest average 5-minute price periods across the NEM”. Yah, biiiiig.

Any significant market volatility will naturally yield plenty of discussion around those high prices. I’ve seen plenty of commentary across different social media platforms — some informed, some rather less so — including variants of “the market is fundamentally broken”.

And within the detailed account of the market dynamics by EnergyByte there were some very strong adjectives — crisis, extreme, dramatic. So you’d be forgiven for thinking that the NEM was stretched to its absolute limit.

Now seems like a good time to talk about the NEM as both a system and a market.

The NEM, a market

The National Electricity Market, is… you’re not going to believe this… a market. Generators — power plants — make offers (aka bids) into the market; and successful generators whose offers are cleared by the market are paid the marginal clearing price (aka dispatch price). This process happens every 5-minutes, 105,120 times per year.2

If you’d like to dive deeper into the mechanics we’ve written about this process in detail before.

Like any market, too much demand and not enough supply typically results in high prices. And yes in reality price setting is vastly more complicated than this — including plenty of times when the market sees volatility during otherwise moderate demand; but it’s still a safe bet that tight supply and demand = volatility.

Winter volatility is not a new feature of the NEM, but as the energy transition progresses the affect of dunkelflaute on market prices is exacerbated; what EnergyByte terms ‘triple C conditions’ — cool, calm, cloudy.

Cold weather drives high electrical demand in the early evening from heating loads as people return from work, cloudy days limit solar generation from contributing to pre-heating or charging of battery systems, and calm conditions ensure wind output is minimal.

In fact a EnergyByte allude to the fact that there’s actually a fourth C in there — correlation. Much of the wind and solar systems are affected by the same weather patterns.

Under these conditions the system is almost entirely reliant on thermal generation — gas and coal units — with modest contributions from the hydro-electric units of Snowy and Tassie.

To build on the idea of ‘triple C conditions’ I would add, somewhat cheekily, that we’re seeing the worst of these high price events occur under 'hextuple C conditions’ — cold, correlated cloudy, calm and coal-fired catastrophe.3

At this time of year the number of coal-fired units on planned outages is minimised and each unplanned outage in the ageing coal-fired fleet further tightens the supply demand conditions, requiring that hole to be filled with open cycle gas peakers… which are by definition expensive (especially so if they are without a gas contract).

And sure enough as noted by EnergyByte a significant number of coal-fired units on unplanned outages was a feature of the recent volatility events in June.

Now, let’s be clear up front — I’m in no way advocating that high market prices are a good thing; I’m also a consumer with electricity bills to pay.4

But high prices, or even extended high prices, are not a ‘broken market’.

They might be a sign of a dysfunctional market, perhaps. In fact that sounds like an excellent fireside chat session at an energy conference where various CEOs could sagely nod in furious agreement about the challenges of high prices and market dysfunction. But high prices are just an output of a market doing market things.

Every time the NEM — an energy-only market no less — experiences significant volatility the peanut galleries of various social media fire off about brokenness. There is nothing fundamentally ‘broken’ about the wholesale price going to the Market Price Cap (or the Market Floor Price for that matter) — it’s an upper bound. The National Electricity Rules also don’t set any requirements on bidding based based on costs, so opportunistic profiteering is allowed (this is a neutral statement, not an endorsement).

In fact, for much of the social media commentariat I would point out that focussing exclusively on volatility is not even the correct metric.

The load-weighted average price is a much more important vital sign of market health, along with contract prices (which yes, are affected by volatility, or technically the risk of volatility).

A final point here is to note that AEMO (as the market operator) is tasked with operating the system in the least cost way, but that means ensuring that dispatch is optimal — not controlling or policing the bids of private participants, which is where high pricing eventuates from.

The NEM, a system

Curiously, in common parlance the NEM also refers to the grid — the system of poles and wires connecting generators to customers.5 Somewhat unusually AEMO is both the market and system operator — many other power systems have distinct roles for a Transmission System Operator and a market operator or power exchanges for trading electricity.

With the majority of social media commentary focussed on high prices one could be forgiven for forgetting that there is a physical grid beneath the market — the demand of customers must be matched in real-time by generation supply, irregardless of prices.6 The physical output of generators and the capacity of transmission lines and interconnectors within and between states serve as hard physical limitations on how the system can operate.

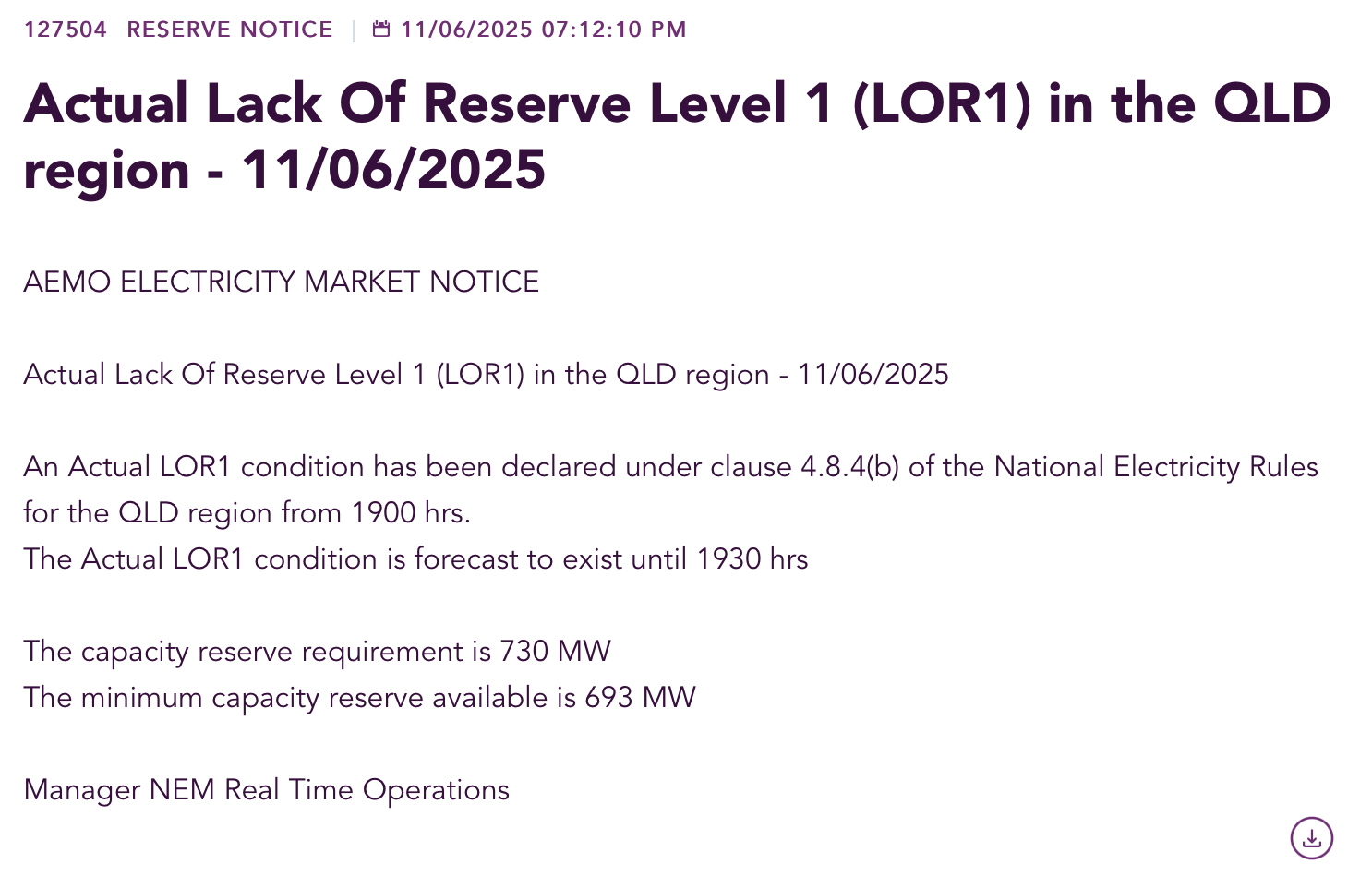

A simplistic guide to assessing the stress on the NEM (the system) is to look at the lack of reserve framework. The LOR framework is based around N-1 contingencies:

LOR1 indicates that there is an N-2 contingency within a given region (after accounting for interconnector capacities). The gap between the available supply and the demand is equal to the two largest online generators. If these two generators were to fall over, there would not be enough supply to meet demand, and load shedding would occur.

LOR2 indicates that there is an N-1 contingency in a given region — the gap between the available supply and the demand is equal to the largest online generator.

LOR3 is load shedding time baby.

AEMO has a system Short Term Projected Assessment of System Adequacy (ST PASA) which forecasts these LOR conditions on a 7-day horizon (forecast LOR). These forecasts serve as both a warning and an incentive — forecast LOR conditions can be an incentive for previously unavailable generators to make their capacity available. It’s worth noting too that forecast LOR conditions don’t always eventuate — demand forecasts are just that, and 7-day forecasts can be as fickle as weather forecasting (in part, because demand is highly weather correlated!)

The LOR framework also enables AEMO to contract out-of-market measures like the Reliability and Emergency Reserve Trader (RERT) which can bring additional non-market generation online, or enable increased demand response.

So, with such extreme, dramatic and extended volatility over the last fortnight, the system must have been stretched to its limit right?

Uhhhh, not quite. In fact, across those three days of volatility Queensland was the only state which barely scraped into LOR1 conditions (the lowest grade) for 30-minutes on the evening of the 11th and for an hour on the morning of the 12th — not the evening when the volatility occurred.

The NEM, a market and a system

The original name for the Market Price Cap should provide some indication of the intention of the upper limit on pricing. The price cap was previously known as VoLL — the Value of Lost Load.7

In economics the value of lost load is the idea of a maximum price that consumers would be willing to pay to avoid disruption to electricity prices. Prices above VoLL suggest that at least some consumers would prefer to stop using electricity rather than pay the premium.

Is the fact that the market price can go to the ceiling and stay there for many hours when the system is not experiencing a dire shortage of generation a sign of a dysfunctional market? Quite possibly, but you’d have to ask the fireside chat participants their views. But neither the market or the system are ‘broken’.8

I’d also like to be clear that I’ve referenced the EnergyByte analysis because it’s easily the most detailed account I’ve seen, but I’m not trying to throw any shade here.

EnergyByte’s analyses are primarily focussed on market outcomes (including the contract markets) and this kind of extended volatility can send under-hedged retailers or market customers to the wall. Which is likely a rather dramatic outcome — crisis even — for those participants.

The third rail

In the discussion of the system above I’ve focussed on generation shortages — reliability. There is another aspect of the NEM (the system) which is extremely important and largely orthogonal to price — security.

The official AEMC definitions of reliability and security are above, but indulge one of my favourite pastimes and whip out some tortured analogies:

Reliability can be likened to petrol in the tank — is there enough to get where you’re going?

Security on the other hand is something more like the suspension and handling — if you hit a nasty pothole, will the car stay straight and true or swerve off the road?

The social media commentariat knows a thing or two about system security — google “Iberian Peninsula black out”. Here in the NEM we had the dramatic South Australian system black in 2016, and a big old wobble in Queensland and New South Wales in August 2018.

Security events are particularly scary because they’re often ‘unknown unknowns’ — that was certainly the case in South Australia where default OEM fault ride through settings on wind farms, unknown to both AEMO and the asset owners, contributed to the system collapse.

As we continue to transition away from a system built around large centralised thermal generation assets, there are going to be some bumps in the road.

In fact there was a particularly prescient quote from the recent Australian Energy Week, where a former senior grid operator made the (slightly pithy but eminently quotable) observation: “Reliability doesn’t scare me. I can always just load shed some customers. System security is what used to keep me up at night.”

So while high prices attract plenty of commentary and yield endless OpenElectricity screenshots, there is a much larger and more complex system underpinning all of that. And determining whether the system is dysfunctional is a much harder task than opining about market volatility.

About a decade ago I was at a winery in Tasmania and the person giving the tasting asked if I was familiar with cool climate wines, to which I replied yes, I know the products of the Yarra Valley well. They responded with a snort and chided me that the Yarra Valley is not. cool. climate. Right now I hope to imagine that there’s a collection of readers arguing over what counts as a ‘southern state’… I shan’t be elaborating.

105,408 in leap years for the pedants in the audience. Or less if the market is under administered pricing… or suspended.

If we were really trying hard to characterise these events we might even class them as Frigid, Overcast, Calm, Correlated, Coal-fired Emergencies, Dark.

In fact, I’ve been on a spot price pass through contract via Amber Electric for the last 4.5 years. I am **acutely** aware of extended high price events.

Our western cousins for example have a clear delineation between the South West Interconnected System — the grid, and the Wholesale Electricity Market.

Yes, this was deliberate. I’m not sorry.

You’ll find old timers and newbies alike still refer to the Market Price Cap as VoLL — it rolls off the tongue much easier I suppose.

I appreciate that in the nuances of language some might take ‘broken’ and ‘dysfunctional’ to be equivalent, but I would point out that the market can actually break — like the market suspension three years ago. Thanks Putin.

Cracking read Alex. You know well that I still call it VoLL.