Line Go Up

But not fun, like meme stocks. Bad, like cholesterol.

Special note — this week’s post is very long. If Gmail truncates it you’ll need to click the view entire message button to read all of it!

Seeing energy prices in the news is like seeing Mel Gibson trending on Twitter — there’s any number of reasons why it might be happening, but it’s almost definitely not good. This time? The announcement that electricity prices are set to surge.1 On Wednesday 15 March, the Australian Energy Regulator released the draft determination for Default Market Offer prices in 2023-24. The final prices will be announced in May, taking effect on 1 July 2023.

So what is the Default Market Offer? Why is it going up? And who does it affect?

We need to start all the way back at how electricity is made.

Just kidding, let’s talk about something more complex — the market.

The Market

Most of the east coast of Australia is connected by the National Electricity Market, which confusingly is both the name of the market, and the name of the system. The NEM is an energy-only market, with wholesale electricity prices unique to each of the five states2 set every 5-minutes of every day.

Energy-only means that this wholesale price is paid to generators (power stations like coal-fired power plants, wind farms, solar farms, etc.) for producing electricity and paid by customers consuming electricity (you, me, the local butcher, the friendly green national hardware chain; you know… us), but only when the power is created or consumed. Paying only for what you use might sound intuitive, but it’s counter to the design of most electricity markets around the world where there are often payments based around the capacity to generate.

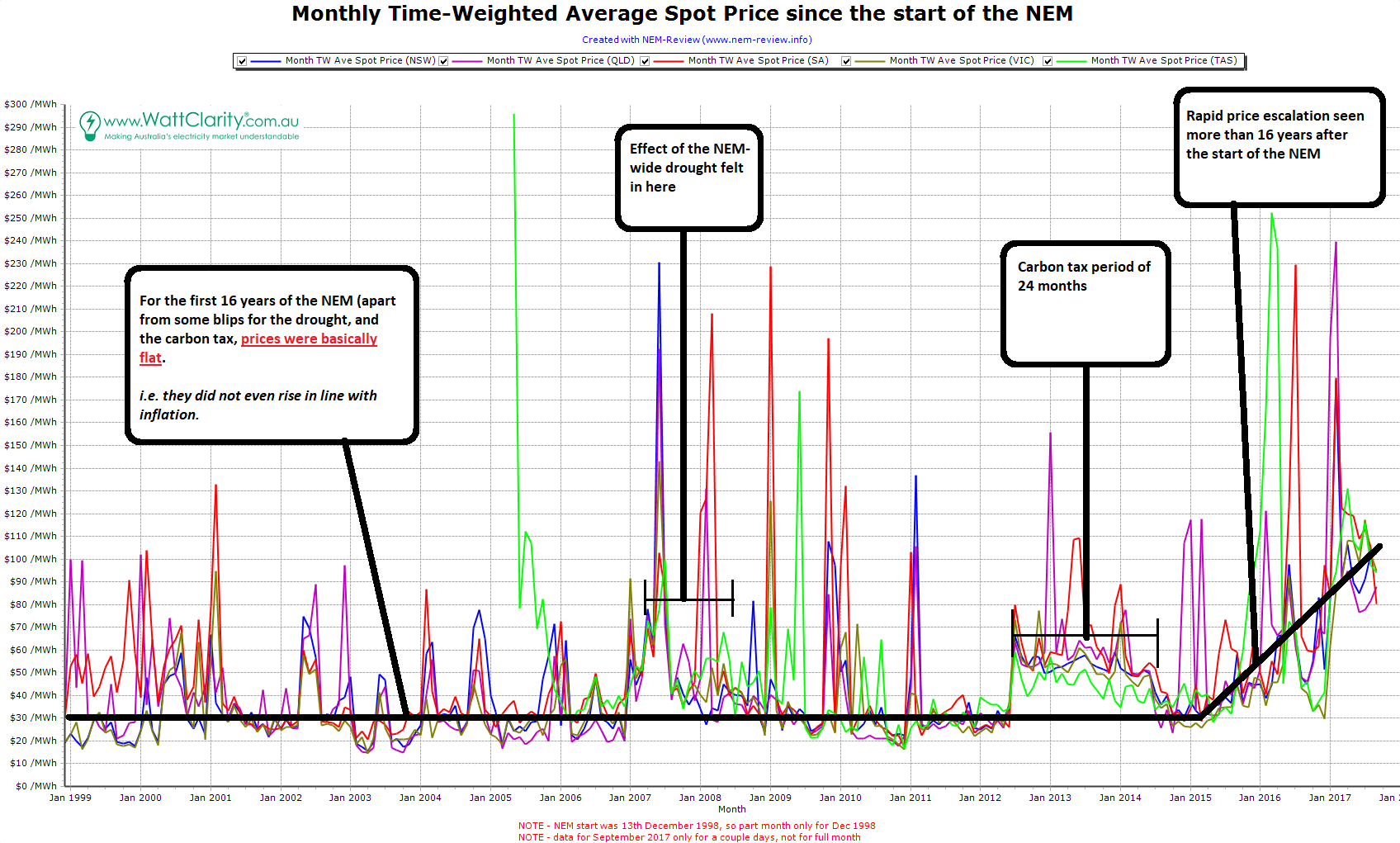

This floating wholesale (or spot) price has limits on how low or high it can go — between -$1,000/MWh and roughly $16,000/MWh3 — but typically it hovers around the $100/MWh mark.4 The price is set by offers into the market and reflects the supply/demand dynamics — tight supply/demand and the price is likely to be high, plenty of supply and low demand and the price will be very low.5 This volatile market, where the upper bound is over 100 times the mean, is actually an important part of the design of an energy-only market, but something to be discussed in more detail another time.

Since the commencement of the NEM in 1998, long term prices were basically flat, minus some bumps — like the widescale drought in 2007 (which affected water used to cool coal-fired power stations and the hydro generators) and the brief carbon tax period. And volatility, particularly during hot summer afternoons or cold winter mornings and evenings has always existed, but by and large things were fairly chill (oooooh, foreshadowing)…

{kind=link}

Except, for the vast majority of us, the price we pay for electricity is very different to the price in the wholesale market. While the prices are related, there are material differences, especially in the short term. This is similar to other markets. Take fruit for an example. Fruit is bought and sold in massive quantities between farms and retailers, and the retailers are responsible for marketing and selling to consumers. In electricity markets, between the wholesale price, and you, is a retailer. Retailers are responsible for measuring your electricity consumption,6 managing the variability of the wholesale spot price and billing you for your usage at an agreed rate.

So, how does this relate to the DMO? It doesn’t yet, cause we’re going to take a detour and talk about risk management, a.k.a “hedging”.

Hedges

The price you and I pay for electricity is typically fixed or flat. That is, we're protected from the variability and volatility of the electricity price in the wholesale market. This creates a challenge for retailers — selling to customers at a relatively fixed price while purchasing from a wholesale market which can be incredibly variable. To manage the potential imbalance, retailers turn to “hedges”.7

There are a range of financial derivatives which exist in order to hedge against the spot price. These are financial instruments traded and managed by the ASX (which acts as the clearing house).

The two main instruments are called swaps and caps.8

A swap is a contract-for-difference product. The buyer and seller agree on a strike price ($/MWh), volume (in MWs) and duration (typically over a year, quarter or month). For every interval where the wholesale price is higher than the strike price, the seller refunds the buyer the difference between the two, and vice versa when wholesale price is below the strike price. The key benefit of a swap is that it allows buyers and sellers to lock in an agreed price in advance. People trade swap contracts out into the future. The prices of these contracts are commonly called “futures prices”, and is seen as broadly reflective of where the average wholesale price will land.9

A cap is an effectively an insurance product. The buyer of a cap pays a premium to lock in a maximum price of electricity (confusingly, also called the strike price). This strike price is typically $300/MWh.

There are also option variants of swaps and caps, where participants have the option to buy or sell an instrument in the future but are not compelled to (i.e. if the wholesale price works out to be better than the hedge).

These instruments are purely financial — buyers and sellers don’t need to actually be generating or consuming electricity, they’re just trading money based on the underlying value of the electricity. This means you can also get financial speculators trading these instruments, effectively making bets on which way electricity prices will go.10

Also, these instruments are bought in blocks — a minimum of a whole month, but typically quarterly,11 or for half years or full years. Trading begins roughly three years in advance, and lasts until a few weeks or months after the delivery period has begun, depending on the length of the contract.

Like spot prices there are state-specific variants for each product, except for Tasmania, which is close enough to a monopoly that trading doesn’t make sense.

The key takeaway is, although the wholesale price for electricity is extremely variable, these hedges allow market participants to be more certain about their wholesale electricity costs.

So what does this have to with retailers?

Retailers

Let’s chat quickly about retailers.

Retailers are responsible for managing the billing of customers. In jurisdictions where full retail competition exists12 customers are free to choose whichever retailer they want. The electrons come from the same place and down the same wires, but there’s a few levers that retailers can pull to create competitive offers, or in some cases the illusion of competitive offers (oooooh, more foreshadowing).

As a customer, your bill consists of six key elements:

Network costs (the costs of distributing electricity down the ‘poles and wires’)

Wholesale costs (the cost of purchasing the electricity from the market — what we’ve been talking about up to now)

Other Market costs (ancillary costs, market fees, fixed costs)

Environmental costs (costs associated with supporting the Renewable Energy Target and state-based schemes)

Hedging costs (risk management costs, often not explicitly itemised)

Retailer margin (usually not explicitly itemised in a bill, that would be bad capitalism)

The first four of these items are outside the control of retailers. As such, the price competitiveness of retailers comes down to how well they manage the last two of theses costs.13 This is fundamental to retail competition in the market.

Retailers make two kinds of offers — market offers and standing offers. Market offers are what you see advertised, and if you change retailer you’ll be signing onto a market offer. Typically, the market offers have the best deals. Standing offers are the default offer — this is the plan you’ll be put on if your market offer expires, if you move into a house and never sign up to a deal, or if your retailer goes out of business and you get transferred to another retailer.

Even for the staunchest believers in the effectiveness of an electricity retail market, market and standing offers had some flaws. Electricity plans are complex, which makes them hard to compare and discourage people from shopping around. For example, market offers were often advertised with insane discounts, but the discount was from an inflated benchmark (and its hard to know what a reasonable benchmark is), giving the false impression of how good the deal was. Customers on standing offers were likely those who were least engaged with the market, meaning they were ripe for getting ripped off by standing offers that were way overpriced compared to the market offers.

So where does the DMO come in?

The DMO

The DMO is relatively new to the NEM. Prior to its existence, the NEM had been ticking along mostly comfortably, with a few minor wrinkles, until November 2016 when Engie announced that they would be closing Hazelwood Power Station in Victoria by March 2017.14 Despite the fact that Hazelwood was extremely old and rather unreliable by this point, this announcement still surprised the market. It was the largest coal-fired station closure during the NEM’s existence (by an order of magnitude) and the four months of notice was very short.

In March 2017, the then treasurer Scott Morrison commissioned the ACCC to publish an inquiry report into electricity pricing in Australia. It was published in June 2018 (not long before he ascended from Treasurer to PM) and one recommendation it made was the creation of a backstop on electricity retail offers.

The premise behind this was that retailers were setting artificially high standing offers in order to provide large discounts against these benchmarks, and cash in on those disengaged customers.

The government accepted this aspect of the ACCC recommendations and tasked the AER with determining a strategy to set a common default price.

Thus was born the Default Market Offer in July 2019 — a maximum default price which retailers can charge customers (and thus by default, most retailer standing offers reflect the DMO).

Note that the DMO doesn’t apply to Tasmania or regional Queensland (which don’t have full retail competition), or Victoria, because Victoria does it themselves. The Essential Services Commission of Victoria sets the Victorian Default Offer which is effectively the same thing but under a different name.

The DMO has a specific methodology (link if you’re a nerd) which takes into account the rolling wholesale energy costs, plus the network costs specific to each network15 and a view to the future price. Importantly, it’s not just the raw futures price, but it has to account for when the hedges may have been purchased.

And so the DMO has become important, not only because it sets a maximum threshold for a how much a customer can be charged for electricity when on a standing offer; but because it is now the benchmark against which everything is set. Offers, discounts and the notional price that customers pay16 are all benchmarked against the DMO.

So, Why is the DMO Increasing?

In short, because of this little guy.

When Russia invaded Ukraine in February last year, western countries sanctioned Russia as punishment. Russia retaliated by limiting natural gas supply, particularly to European countries, which drove up international gas prices. Because Australia’s gas price is export linked, our domestic gas price shot up. At the same time there were was a much larger than normal number of coal-fired power stations offline for unexpected maintenance (as well as lower solar and wind generation typical of early winter), which meant the electricity market relied heavily on gas fired power stations to meet the demand. Many of these gas stations didn’t have enough contracted gas purchased in advance, and so had to buy gas from the gas spot market, at very high rates, which led to electricity prices becoming very high, particularly in May and June (record highs for the NEM, actually).

Many retailers had to buy electricity at this spot rate, even though their customers are paying fixed rates agreed long in advance. Unsurprisingly, a few of these retailers didn’t survive.

Because the DMO for FY2022 was determined prior to the worst of these wholesale events, much of the impact on this current DMO are the events of May/June 2022 are still coming home to hurt us. This is because the hedges bought by retailers have significantly increased in price, and the methodology for setting the DMO is based on these hedging costs.

Additionally, both gas and coal prices are still fairly high. So there’s an expectation that while wholesale prices have come off the boil relative to 2022, they’ll still remain moderately high for a while yet.

Conclusion

If you’ve made it this far, wow. Gold star. Get yourself some new gumboots because you have done some good wading.

Hopefully we’ve been able to shed a little bit of light on the complexities behind why line go up and how events close to 12 months old are still making line go up.

And while you’re unlikely to actually pay the DMO, much like home loans, if you’re rolling off an expired contract and renewing electricity offers or signing up to a new retailer, line. go. up.

Things happen

On Friday the Productivity Commission released the mammoth Productivity Inquiry 2023, which among many, many things, recommended the government expand the Safeguard Mechanism in order to meet Net Zero targets and rethink subsidies for renewables and EVs. It’s almost like carbon taxes are the most effective way of curbing emissions…

The sale of the very, very large solar farm and very, very long cable has attracted multiple potential buyers. This throws some interesting doubt on the assumption that the project would be scooped up by either Twiggy or MCB.

AEMO’s dire warnings of winter natural gas shortfalls have been cast into doubt with the announcement that the Queensland LNG exporters have earmarked supplies to provide the domestic market.

Not our pun. But of course we’re going to repeat it.

Despite being the seat of the nation’s capital, the ACT doesn’t get any special treatment and it just gets bundled into NSW.

This upper limit is indexed roughly to inflation and increases in July each year.

The technical name for this is mean-reverting stochastic volatility. This is really not relevant to the article, but can we just appreciate how beautiful that phrase is.

This is a gross over-simplification, but this article is already long enough without getting sidetracked into generator bidding dynamics.

ACTUALLY IT’S THE METERING DATA PROVIDER WHO IS RESPONSIBLE FOR DOING THE MEASURING PLEASE DON’T @ ME ENERGY PROFESSIONALS.

There’s a fairly good, if dry, article here explaining in more detail how retailers typically use hedges.

These hedges, and specifically swaps and caps, are not the only ways retailers can manage risk or pricing volatility. But swaps and caps are the most commonly used, widely traded and discussed in terms of market analysis.

The futures price is particularly important — swaps are openly traded, and the value (i.e. the strike price) goes up and down over time. Much like stocks, there are humans behind these trades responding to events and announcements regarding the energy market, or global events, or sometimes just weird jitters.

This isn’t unique to electricity. The Big Short has a nice layperson explanation of how financial speculators loaded up on mortgage debts.

Very common for caps.

Anywhere other than Tasmania and regional (outside of the south east) Queensland.

There are other ways retailers can make a more competitive offer, such as renewables-backed, supplying goodies like hardware, Kayo subscriptions or nice apps, good customer services, bundling with other utility services like internet etc.

This event turned out to be a something of trigger for a whole range of energy market reforms, but we’re getting ahead of ourselves.

So the DMO is actually a series of 5 different prices for the distribution networks and regions covered by the AER — South Australia, South East Queensland and three distributors in NSW.

And used to produce headlines like “power prices increase by 31%”