We know what you really wanted opening an email called “Get Low”. Take five, click the link, and enjoy some tunes from France's best musical export.1

Ok, now that we've got that out of all our systems, let's get lower and talk about negative pricing.

The NEM is an energy-only regional mandatory gross pool market (I swear my computer just auto-completed that sentence). Ok, ok, ok, that’s a bit obtuse. Let’s break it down.

What it means is all energy must be bought and sold, in real time, from the pool, at the regional price (the spot price). You can't avoid paying (or earning) this price (although there are secondary markets for financial derivatives based on this price). This will be important later…

The spot price for electricity has a floor and cap, codified in the National Electricity Rules. The Market Price Cap2 is indexed to inflation and ratchets up each year in July. It's currently set at $16,600/MWh.

There's also a floor price, the Market Floor Price.3 It is currently, and has always been, set at -$1,000/MWh. It does not adjust annually with inflation.

What does a negative price mean?

Quite literally that generators have to pay for the privilege of generating.

Which means the inverse holds true right? That loads could be paid to consume electricity? Yep! But more on that later.

But Whyyyyyyyy?

Let's take a step back.

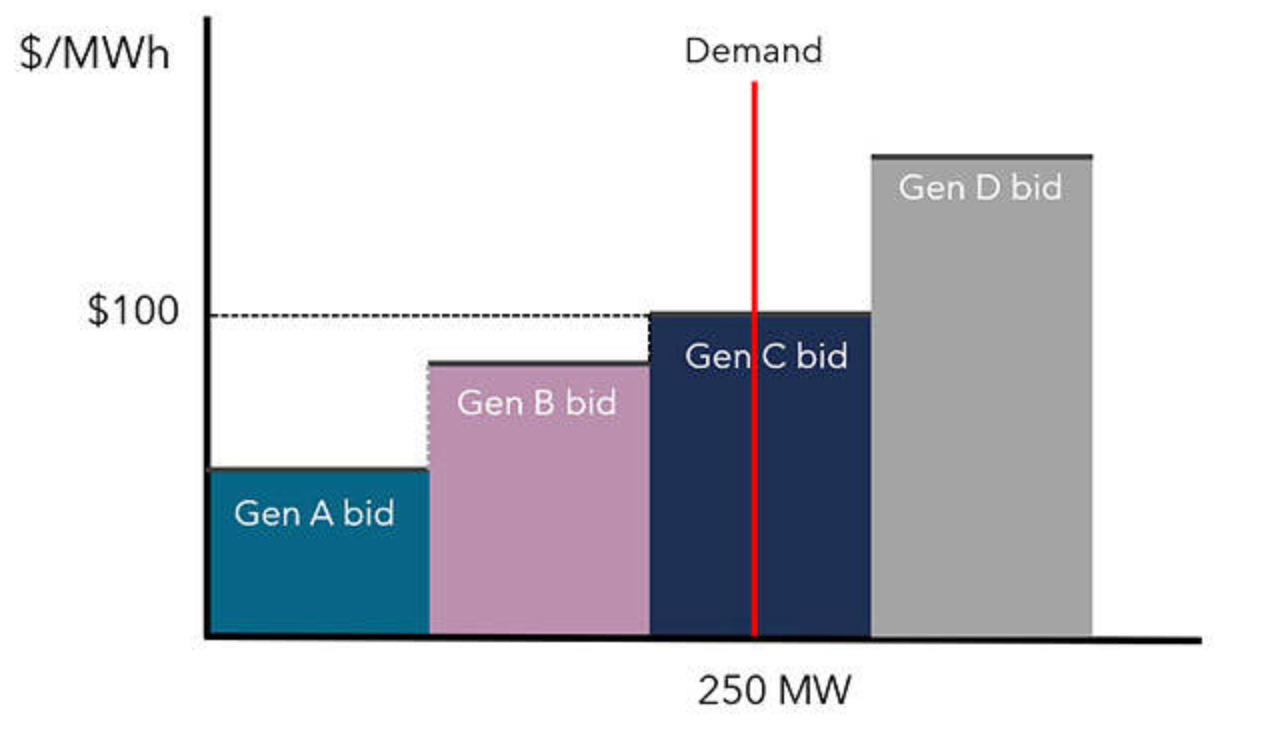

This regional gross pool price is not set by AEMO, or the AEMC, or the energy minister or even DJ Snake (sadly). It's set by good old fashioned markets, baby. Generators bid (offer) into the market in order to be dispatched. The volumetric sum (in Megawatts) of these offers are stacked, from cheapest to highest.4 The resulting price is the cheapest bid which meets the volumetric demand of the region. This is called the marginal bid. This process happens every 5-minutes, of every day, of every year.5

Now, before we proceed, we have to talk about coal-fired generation. Specifically, some important characteristics of coal-fired units which are relevant to our discussion:

They prefer to run mostly flat out (high capacity factors). Like most combustion-driven processes, the efficiency of coal-fired units is non-linear, and is more efficient at power outputs closer to their maximum.6

Coal-fired units have a minimum output – they can’t produce any power below this threshold and need to be switched off.

It's very hard to switch coal-fired units off. Actually, that's not true, it's pretty easy to switch them off. It's hard to turn them back on. Hot starts are usually several hours and cold starts can be 24 hours or more from flicking the ON switch to grid synchronisation.

So, we have a system where there is more generation capacity then average demand, and a bunch of generators clamouring to provide power (and be paid). The NEM was formed in the 1990s, so the majority of this clamouring is from coal-fired units, who would like to avoid switching off the reasons outlined above.

What's the solution? Allow generators to bid at negative prices, which signals to the market just how keen they are to remain operating. If the demand is extremely low, and everyone is bidding at negative prices, then the resulting market price will be negative.

Negative prices serve as an economic disincentive to generate.

Why not just zero? Because we need some of these units to switch off (they can’t each just ramp down to some arbitrarily low number, because of that pesky minimum threshold). So there has to be some kind of disincentive to not generate in the first place.

So, negative prices were originally a way of dealing with over-supply of thermal generation in an energy-only market.7

Getting Low

So if negative bids (and corresponding prices) have always been a feature of the NEM, why are they such a topic recently?

The story can be told in two charts.

The first chart shows the occurrence of dispatch (5-minute) negative prices, expressed as a percentage of the total time for the month.

And yep, that’s a lot of negative prices these days. All regions except for New South Wales are routinely seeing months where the spot price is negative for 10-30% of the entire month. The worst affected months are typically during spring and autumn, but we’ll get to that in a bit.

And here’s the second chart. The chart below shows the half-hourly occurrence of negative prices on each day of the year for three different years (2013, 2015, 2022). The colours indicate the depth of the negative price — darker colours are more deeply negative.

I’ve selected to chart South Australia because it is the most extreme example, but the same trends are broadly occurring across all regions.

Not only is the frequency of occurrence increasing, but the timing or pattern of occurrence has clearly shifted – prices are consistently negative in the middle of the day, year round.

But coal-fired plant have always been bidding at negative prices, why haven’t we seen significant negative prices historically? For one, because the price is pay-as-cleared, not pay-as-bid. The bid of the marginal generator (i.e. the cheapest bid required to meet demand) is the one that sets the price for everyone. And historically, the marginal price has been positive.

So, what else has changed?

So why are they getting lower?

There are two fundamental causes — the rise of rooftop PV and the increase in grid-scale renewable generation. Both of these phenomenon really exploded, you guessed it, around 2016.

The chart below is adapted from the Australian Photovoltaic Institute’s data on cumulative rooftop PV installations. It’s goddamn meteoric. There’s around 32 GW of rooftop PV capacity currently installed in the NEM. For some context, that’s about the same as the all time peak demand of the NEM.8

This next chart shows the other side of the equation which is the installed capacities of grid-scale stuff. Wind is a more mature technology and has been steadily growing since at least 2010, but things got properly hectic with the explosion of grid-scale solar from 2018.9

Apart from the sheer scale and rapidity of the growth of renewables, there’s two important points to note here.

Rooftop solar reduces demand and excess (i.e. solar not consumed by the household) is exported into the grid. Rooftop solar is not dispatched (i.e. it doesn’t bid into the market), it just does its thing whenever the sun shines. The net result is that increasing rooftop solar reduces the demand on the system required to be met by other generation. This is most apparent during spring and autumn when we’re just sipping juice from the grid (mild days means minimal heating and cooling load) and the sky is clear and sunny.

The rise of utility scale renewables has largely come from a new type of participant.10

These newer participants building renewable generation were looking to do it as cheaply as possible. Unlike a coal-fired power plant which is a finely tuned machine operating on a knife-edge and requires a team of operators to keep it running at all times, wind and solar farms largely just sit in a paddock and generate, no operators required.

But the NEM requires that these assets bid into the market, that’s how the market works right? So, put your economically rational hat on — how do you manage the bidding of your plant such that you can effectively take your hands off the wheel?

Yep. You bid the plant at the floor (-$1,000/MWh) all the time. The NEM pays as clears, so you’ve guaranteed that you’re at the bottom of the bidstack and you’ll be paid whatever the marginal generator price is.

And it worked for a while. Quite a while. No shade, it’s the economically rational decision.11 But as the installed capacity of solar and wind farms continued to climb, it started working not so well. And the inevitable outcome is that the price starts creeping into negative territory.

Even then for a while things were fine — because a lot of the early solar and wind farms were financed with PPA offtakes. A Power Purchase Agreement is typically a contract with a counter-party who agrees to buy all or some of your generation output at an agreed fixed price. But remember how I said the NEM is a gross pool energy-only market? These contracts can’t exist right? Well, they can, but only in a purely financial sense. So when the wind or solar farm is generating and the spot price is negative, the offtaker is actually having to pay that price to AEMO. The solar or wind farm owner is home clear because they already negotiated a fixed price! They’re not actually worried about the spot price.

Eventually the chickens were always going to come home to roost.

The Rise of Curtailment

For one thing, no-one is still writing PPA contracts without clauses which explicitly deal with negative prices. Everyone learned that lesson.

There’s two very clear patterns occurring right now:

Semi-scheduled generators12 are now bidding more strategically, i.e. not just at the floor price all the time. They were always able to do this, but it was economically rational not to bother. But now they need a trading team (typically outsourced to specialised organisations for cost reasons) and/or bidding algorithms to actively manage their bids. This is a good thing! The economic disincentives work, and force participants to modify their behaviours.

Non-scheduled generators, who don’t bid into the market, are still doing economic curtailment by switching off when the price goes negative. This is slightly less good, because the behaviour is more opaque to the System Operator (AEMO) — did the solar farm switch off because of low pricing, because cloud cover drifted over the solar farm or because a crazed retired geologist13 stormed the premises and started vandalising panels? It’s not always easy to know.

When the negative prices occur, they’re closely aligned to the value of Large-scale Generation Certificates.

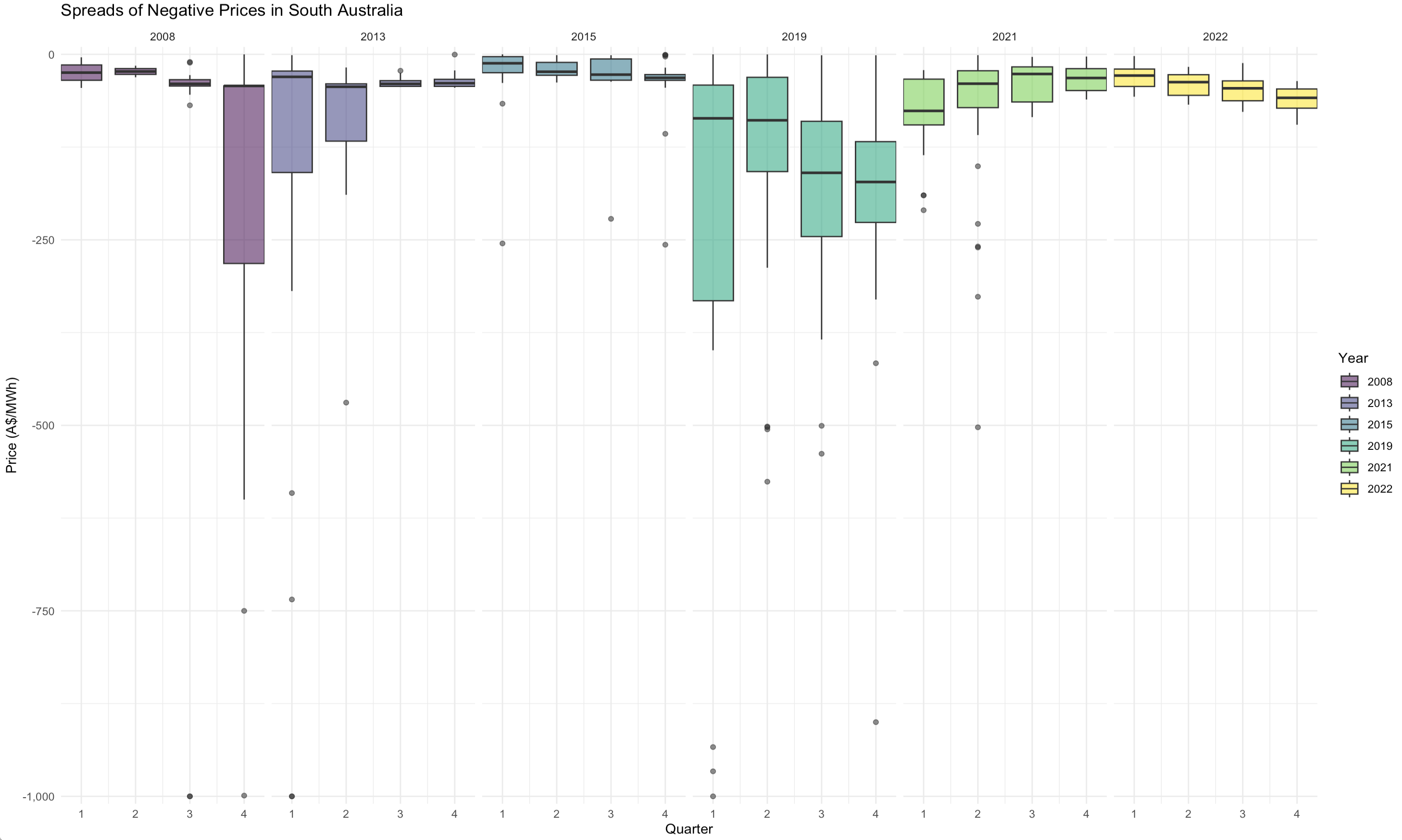

The chart below shows the distribution of quarterly negative prices in South Australia over several years. In previous years the majority of the negative prices might lie in the -$250-0/MWh range, but from 2021 onwards the prices are very tightly in the -$100-0/MWh range.

This is the influence of LGCs, Australia’s primary environmental certificate. Utility-scale (and large commercial rooftop PV systems) renewable projects are eligible for LGCs. Historically the price of these certificates has been between $30-60/MWh. So the breakeven generation price for renewable generation is between -$30/MWh and -$60/MWh. The individual bidding characteristics and LGC price threshold will vary between generators, but the pattern in aggregate is very clear – wind and solar farms are bidding at a price where they don’t lose money.

So, what now?

So, if we’re continuing to build both grid-scale renewables and rooftop PV at pace, where do we go from here?

This is a trickier topic worthy of its own article, but in summary the rise of negative prices (driven by the underlying change in the shape of generation) will drive changes in consumption patterns. Contrary to the opinions of the LinkedIn peanut gallery, this is what a market does (literally, by design).

Remember how loads are paid to consume from the grid during negative prices? Storage (typically Li-Ion batteries, but also pumped hydro-electric generators and other novel forms of storage) is able to benefit from this by charging during the negatively priced periods in the middle of the day and discharging into the (positively priced) system peaks. Negative prices increase the intraday spreads that these assets can arbitrage.

Increasingly demand is becoming more and more flexible to take advantage of these periods too — electric vehicles can be charged during the middle of the day and other loads can be more flexible.14 This could be as simple as shifting time-independent loads (does it really matter when the dishwasher runs, so long as it does run on a daily basis?), or restructuring bigger loads (factories may have previously done things overnight to take advantage of low prices might be able to modify schedules).

But, these things are not without challenges.

For one, sometimes it isn’t actually that simple to just shift a load — there’s a limit to how much can be shifted. And suggesting that manufacturing can readily restructure its scheduling is rather hand wavey.

Secondly, there’s another pricing impediment. Network tariffs, the cost of using the poles and wires, are not currently zero (or negative) in the middle of the day.15 This works to lower the negative price threshold at which a load would be paid to consume — i.e. if the spot price is -$50/MWh and the network tariff is 6c/kWh ($60/MWh), then you’re still paying $10/MWh to charge. This is a low rate, but it’s not the same as getting paid to consume.

In order for loads to take advantage of negative prices, we need structural changes to network tariffs, which is happening, but slowly.

Longer term, the concept of deeply negative prices largely isn’t sustainable – for one, there’s nothing preventing renewable generators from increasing their bids (offers) closer to zero, or above zero. In a world where the system is entirely renewable, or close to, this is the only rational outcome. When (if) the Renewable Energy Target (RET) ends in 2030, taking LGCs with it, this will be especially true. For two, unlike coal plants wind and solar farms can be simply switched off – the economics of negative prices plays out differently.

The fundamental point I’d like to drive home here is that negative prices are a result of renewables, only in the sense that renewables to date have been bidding in an economically rational manner. Renewables ≠ negative prices in and of themself. Negative prices are purely an outcome of how the bidding and dispatch market rules work.

Things Happen

The Federal government has expanded the Capacity Investment Scheme, signalling investment support for 23 GW of VRE and 9 GW of dispatchable generation via a collared underwriting mechanism. This the big governmental push required to get Australia somewhat back on track to meet our decarbonisation targets.

John Birmingham’s reporting of Tony Abbott’s recent address to the IPA might not be quite a faithful retelling of the narrative (but it’s not wrong either).

Did you know Tamworth was the first city in Australia with electric streetlights across the whole town, 135 years ago? There’s a museum you can drag your unwilling spouse and children along to too, because what’s a family holiday without energy tourism?

Ooooooh that got you riled up. You thought it was gonna be Daft Punk, Air, Phoenix… maybe M83? Yelle, you thought I was gonna say Yelle? Wrong. It's DJ Snake.

Previously known as the Value of Lost Load or VoLL. Old timers still call it VoLL, as do Zoomers who’ve rediscovered smoking. To be fair “vol” rolls off the tongue more readily than MPC.

What was wrong with “Market Price Floor”?

The realities of price setting are actually wildly more complex, but the core concept is based on the idea of merit order dispatch. There’s lots more detail about price setting in the NEM here, if that’s of interest.

Except for times when the NEM shits itself, which occurs rather more frequently than you'd like.

Incredibly, the police will not accept this fuel efficiency argument for gunning it down the highway flat out.

In a capacity market, most of the thermal generation has already received some form of capacity payment, which which alters the economics somewhat.

Yes, yes. Don’t @ me. I know that’s now how that works. But it is useful to think about the scale here.

What’s hidden in this chart is the generation mix by region. South Australia and Victoria have had more wind earlier than the other states. Hence the occurrence of negative prices was not uniform across the regions until recently.

At least, compared to the ownership model of the incumbent thermal and hydro-electric generators, which are dominated by only half a dozen companies.

And to be clear I’m not arguing for higher operational costs here.

I haven’t actually explained, but the simplification is: In the very early days of wind (utility scale solar wasn’t on the scene), AEMO allowed these generators to be ‘non-scheduled’ – they didn’t have to bid into the market (or participate in other market processes), they would just generate whenever the wind blew. It fairly quickly became clear this wasn’t a great idea, so the semi-scheduled category was introduced in 2008. Semi-scheduled generators need to comply with the AEMO market processes, including bidding, but with the understanding that if the wind blows less than anticipated then there’s not a tonne they can do.

“Anthropogenic climate change is a lie, it’s sun cycles and other stuff. I saw a great YouTube video explaining it.”

Residential hot water is a big one – it constitutes roughly a third of residential energy consumption.

There are a handful of network tariffs with ‘solar soaker’ periods, and a handful more currently being trialled, but honestly this is a bit of a sore point given the pace of change underway.

This was a fun read, thanks Alex!

Another cracker thanks Alex always appreciate your insights and wit.